Average UK Pension Pot: How Much You Need for a Comfortable Retirement in 2026 (Full UK Income & Savings Guide)

The average UK pension pot has become one of the most searched financial topics in 2026, as people increasingly worry about whether they are saving enough for retirement. A pension pot represents the total savings built through workplace schemes, private pensions, and investment growth over time. However, the average UK pension pot varies widely across the population, meaning it can only ever act as a rough benchmark rather than a guaranteed retirement figure.

In reality, the average UK pension pot does not reflect the true financial needs of most individuals approaching retirement. Many workers assume that a mid-range pension balance will provide long-term comfort, but rising inflation and living costs often reduce its real value. Understanding how pension savings connect with salary levels, lifestyle expectations, and state support is essential for building a realistic retirement strategy in the UK.

What Is the Average UK Pension Pot in 2026?

The average UK pension pot in 2026 is commonly estimated between £80,000 and £110,000 depending on data sources, age groups, and whether figures are calculated using median or mean values. This range reflects the overall savings of UK adults with pension access, but it can be misleading because a small number of high-value pots significantly increases the average figure.

The average UK pension pot also hides a deeper issue: many people have far less than they expect. While some retirees may hold substantial savings, a large proportion of workers still have modest pension balances. This means the average UK pension pot should be viewed as a statistical reference point rather than a reliable indicator of financial readiness for retirement in the UK.

Average UK Pension Pot by Age Group

The average UK pension pot varies significantly across different age groups, reflecting how long individuals have been contributing to their retirement savings. Younger workers often start with small balances, sometimes only a few thousand pounds, while those in mid-career see gradual growth as employer contributions and compound interest begin to build momentum over time.

By the time individuals reach their late 50s or early 60s, the average UK pension pot can exceed £100,000, although this still may not be enough for a long retirement. The key takeaway is that time in the market matters more than income alone, and starting early can dramatically improve the final pension outcome compared to those who delay saving.

Average UK Salary, Wage and Income vs Pension Contributions

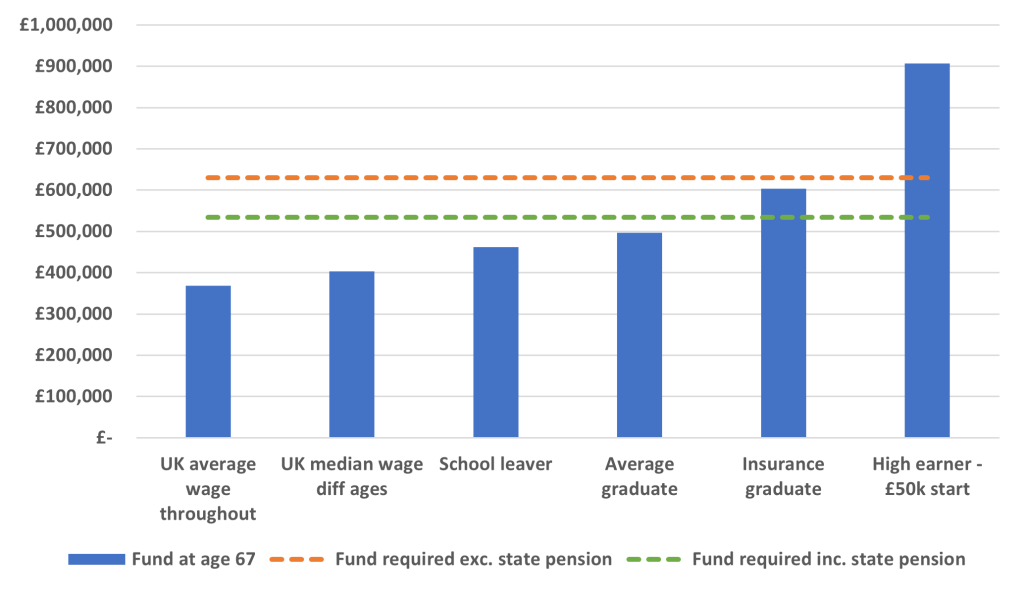

The average UK salary plays a crucial role in shaping pension outcomes, as contributions are usually calculated as a percentage of earnings. In 2025 and 2026, the average UK wage continues to vary across industries, regions, and job roles, which means pension growth is uneven across the population. Higher earners naturally build larger pension pots, while lower-income workers often struggle to contribute consistently.

Despite steady increases in the average UK salary, the average UK pension pot does not always reflect this growth. Many individuals fail to increase contributions in line with pay rises, meaning their retirement savings lag behind their earning potential. This disconnect highlights the importance of actively managing pension contributions rather than relying solely on automatic enrolment systems.

What Is a Comfortable Retirement in the UK?

A comfortable retirement in the UK is generally defined as having enough income to cover essential living costs, leisure activities, and unexpected expenses without financial stress. This level of retirement lifestyle typically requires significantly more than what the average UK pension pot can provide on its own, especially when considering longer life expectancy and rising costs.

Financial experts often suggest that retirees may need between 50% and 70% of their pre-retirement income to maintain a comfortable standard of living. When comparing this target with the average UK pension pot, it becomes clear that many individuals may need additional savings, investments, or part-time income to achieve financial stability throughout retirement.

Cost of Living Factors That Impact Pension Needs

The cost of living in the UK has a direct and powerful impact on how far the average UK pension pot can stretch during retirement. Everyday expenses such as housing, energy bills, transport, and healthcare continue to rise, reducing the real value of fixed pension income over time. This makes long-term planning essential for financial security.

Factors such as average UK house prices, mortgage rates, and utility costs all influence retirement affordability. Even small increases in living expenses can significantly affect retirement budgets. As a result, the average UK pension pot must be considered alongside inflation trends and regional cost differences to understand its true purchasing power in later life.

UK Savings Behaviour and Financial Preparedness

Savings behaviour in the UK shows that many households are not fully prepared for retirement, with the average UK pension pot often falling below recommended levels. A significant number of people prioritise short-term financial needs over long-term retirement planning, which leads to insufficient pension growth over time.

The average UK savings rate also highlights a broader issue of financial discipline. While some households maintain consistent contributions to pensions and investment accounts, others struggle to save at all due to rising costs and debt pressures. This imbalance plays a major role in shaping the overall retirement readiness of the UK population.

How Much You Should Aim for in Your Pension by Retirement

Financial planners often suggest that individuals aim for a pension pot that is 8 to 12 times their annual income, depending on retirement age and lifestyle expectations. This target is significantly higher than the average UK pension pot, which means many people may need to increase contributions or delay retirement to bridge the gap.

Building towards this goal requires consistent long-term planning, including increasing contributions during peak earning years and taking advantage of employer matching schemes. When compared with the average UK pension pot, these strategies highlight how proactive saving can dramatically improve retirement outcomes and financial independence.

How to Increase Your UK Pension Pot Faster

Increasing your pension pot requires a combination of discipline, strategy, and long-term thinking. One of the most effective methods is to raise contribution percentages whenever income increases, ensuring that retirement savings grow alongside earnings rather than remaining static. This approach helps individuals move beyond the limitations of the average UK pension pot.

Other strategies include consolidating old pensions, maximising tax relief benefits, and investing in growth-focused funds. Over time, compound interest plays a major role in expanding savings. By actively managing pension accounts, individuals can significantly outperform the average UK pension pot and build stronger financial security for retirement.

Conclusion: Are You On Track for a Comfortable Retirement?

The average UK pension pot provides a useful reference point, but it does not guarantee financial comfort in retirement. Many people assume their savings are sufficient until they compare them with actual retirement costs, which often reveal a significant shortfall. Understanding this gap early is essential for building long-term financial stability.

Ultimately, achieving a comfortable retirement requires more than relying on the average UK pension pot. It demands consistent saving, informed financial decisions, and a clear understanding of future living costs. By taking proactive steps today, individuals can improve their retirement outcomes and create a more secure financial future in the UK.

You may also read: Evolution of Scooby-Doo Characters Over Time